A credit default swap (CDS) is a financial swap agreement that the seller of the CDS will compensate the buyer in the event of a debt default (by the debtor) or other credit event.[1] That is, the seller of the CDS insures the buyer against some reference asset defaulting. The buyer of the CDS makes a series of payments (the CDS "fee" or "spread") to the seller and, in exchange, may expect to receive a payoff if the asset defaults.

In the event of default, the buyer of the CDS receives compensation (usually the face value of the loan), and the seller of the CDS takes possession of the defaulted loan or its market value in cash. However, anyone can purchase a CDS, even buyers who do not hold the loan instrument and who have no direct insurable interest in the loan (these are called "naked" CDSs). If there are more CDS contracts outstanding than bonds in existence, a protocol exists to hold a credit event auction. The payment received is often substantially less than the face value of the loan.[2]

Credit default swaps in their current form have existed since the early 1990s, and increased in use in the early 2000s. By the end of 2007, the outstanding CDS amount was $62.2 trillion,[3] falling to $26.3 trillion by mid-year 2010[4] and reportedly $25.5[5] trillion in early 2012. CDSs are not traded on an exchange and there is no required reporting of transactions to a government agency.[6] During the 2007–2010 financial crisis the lack of transparency in this large market became a concern to regulators as it could pose a systemic risk.[7][8][9] In March 2010, the Depository Trust & Clearing Corporation (see Sources of Market Data) announced it would give regulators greater access to its credit default swaps database.[10]

CDS data can be used by financial professionals,[11] regulators, and the media to monitor how the market views credit risk of any entity on which a CDS is available, which can be compared to that provided by the Credit Rating Agencies. U.S. Courts may soon be following suit.

Most CDSs are documented using standard forms drafted by the International Swaps and Derivatives Association (ISDA), although there are many variants.[7] In addition to the basic, single-name swaps, there are basket default swaps (BDSs), index CDSs, funded CDSs (also called credit-linked notes), as well as loan-only credit default swaps (LCDS). In addition to corporations and governments, the reference entity can include a special purpose vehicle issuing asset-backed securities.[11][12]

Some claim that derivatives such as CDS are potentially dangerous in that they combine priority in bankruptcy with a lack of transparency. A CDS can be unsecured (without collateral) and be at higher risk for a default.

Description

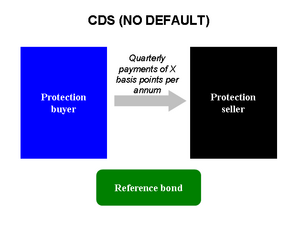

A CDS is linked to a "reference entity" or "reference obligor", usually a corporation or government. The reference entity is not a party to the contract. The buyer makes regular premium payments to the seller, the premium amounts constituting the "spread" charged in basis points by the seller to insure against a credit event. If the reference entity defaults, the protection seller pays the buyer the par value of the bond in exchange for physical delivery of the bond, although settlement may also be by cash or auction.[7][13]

A default is often referred to as a "credit event" and includes such events as failure to pay, restructuring and bankruptcy, or even a drop in the borrower's credit rating.[7] CDS contracts on sovereign obligations also usually include as credit events repudiation, moratorium, and acceleration.[6] Most CDSs are in the $10–$20 million range[14] with maturities between one and 10 years. Five years is the most typical maturity.[11][12]

An investor or speculator may "buy protection" to hedge the risk of default on a bond or other debt instrument, regardless of whether such investor or speculator holds an interest in or bears any risk of loss relating to such bond or debt instrument. In this way, a CDS is similar to credit insurance, although CDSs are not subject to regulations governing traditional insurance. Also, investors can buy and sell protection without owning debt of the reference entity. These "naked credit default swaps" allow traders to speculate on the creditworthiness of reference entities. CDSs can be used to create synthetic long and short positions in the reference entity.[8] Naked CDS constitute most of the market in CDS.[15][16] In addition, CDSs can also be used in capital structure arbitrage.

A "credit default swap" (CDS) is a credit derivative contract between two counterparties. The buyer makes periodic payments to the seller, and in return receives a payoff if an underlying financial instrument defaults or experiences a similar credit event.[7][13][17] The CDS may refer to a specified loan or bond obligation of a "reference entity", usually a corporation or government.[14]

As an example, imagine that an investor buys a CDS from AAA-Bank, where the reference entity is Risky Corp. The investor—the buyer of protection—will make regular payments to AAA-Bank—the seller of protection. If Risky Corp defaults on its debt, the investor receives a one-time payment from AAA-Bank, and the CDS contract is terminated.

If the investor actually owns Risky Corp's debt (i.e., is owed money by Risky Corp), a CDS can act as a hedge. But investors can also buy CDS contracts referencing Risky Corp debt without actually owning any Risky Corp debt. This may be done for speculative purposes, to bet against the solvency of Risky Corp in a gamble to make money, or to hedge investments in other companies whose fortunes are expected to be similar to those of Risky Corp (see Uses).

If the reference entity (i.e., Risky Corp) defaults, one of two kinds of settlement can occur:

- the investor delivers a defaulted asset to Bank for payment of the par value, which is known as physical settlement;

- AAA-Bank pays the investor the difference between the par value and the market price of a specified debt obligation (even if Risky Corp defaults there is usually some recovery, i.e., not all the investor's money is lost), which is known as cash settlement.

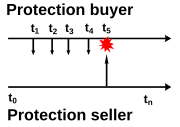

The "spread" of a CDS is the annual amount the protection buyer must pay the protection seller over the length of the contract, expressed as a percentage of the notional amount. For example, if the CDS spread of Risky Corp is 50 basis points, or 0.5% (1 basis point = 0.01%), then an investor buying $10 million worth of protection from AAA-Bank must pay the bank $50,000. Payments are usually made on a quarterly basis, in arrears. These payments continue until either the CDS contract expires or Risky Corp defaults.

All things being equal, at any given time, if the maturity of two credit default swaps is the same, then the CDS associated with a company with a higher CDS spread is considered more likely to default by the market, since a higher fee is being charged to protect against this happening. However, factors such as liquidity and estimated loss given default can affect the comparison. Credit spread rates and credit ratings of the underlying or reference obligations are considered among money managers to be the best indicators of the likelihood of sellers of CDSs having to perform under these contracts.[7]

Differences from insurance

CDS contracts have obvious similarities with insurance contracts because the buyer pays a premium and, in return, receives a sum of money if an adverse event occurs.

However, there are also many differences, the most important being that an insurance contract provides an indemnity against the losses actually suffered by the policy holder on an asset in which it holds an insurable interest. By contrast, a CDS provides an equal payout to all holders, calculated using an agreed, market-wide method. The holder does not need to own the underlying security and does not even have to suffer a loss from the default event.[18][19][20][21] The CDS can therefore be used to speculate on debt objects.

The other differences include:

- The seller might in principle not be a regulated entity (though in practice most are banks);

- The seller is not required to maintain reserves to cover the protection sold (this was a principal cause of AIG's financial distress in 2008; it had insufficient reserves to meet the "run" of expected payouts caused by the collapse of the housing bubble);

- Insurance requires the buyer to disclose all known risks, while CDSs do not (the CDS seller can in many cases still determine potential risk, as the debt instrument being "insured" is a market commodity available for inspection, but in the case of certain instruments like CDOs made up of "slices" of debt packages, it can be difficult to tell exactly what is being insured);

- Insurers manage risk primarily by setting loss reserves based on the Law of large numbers and actuarial analysis. Dealers in CDSs manage risk primarily by means of hedging with other CDS deals and in the underlying bond markets;

- CDS contracts are generally subject to mark-to-market accounting, introducing income statement and balance sheet volatility while insurance contracts are not;

- Hedge accounting may not be available under US Generally Accepted Accounting Principles (GAAP) unless the requirements of FAS 133 are met. In practice this rarely happens;

- To cancel the insurance contract, the buyer can typically stop paying premiums, while for CDS the contract needs to be unwound.

Risk

When entering into a CDS, both the buyer and seller of credit protection take on counterparty risk:[7][12][22]

- The buyer takes the risk that the seller may default. If AAA-Bank and Risky Corp. default simultaneously ("double default"), the buyer loses its protection against default by the reference entity. If AAA-Bank defaults but Risky Corp. does not, the buyer might need to replace the defaulted CDS at a higher cost.

- The seller takes the risk that the buyer may default on the contract, depriving the seller of the expected revenue stream. More importantly, a seller normally limits its risk by buying offsetting protection from another party — that is, it hedges its exposure. If the original buyer drops out, the seller squares its position by either unwinding the hedge transaction or by selling a new CDS to a third party. Depending on market conditions, that may be at a lower price than the original CDS and may therefore involve a loss to the seller.

In the future, in the event that regulatory reforms require that CDS be traded and settled via a central exchange/clearing house, such as ICE TCC, there will no longer be "counterparty risk", as the risk of the counterparty will be held with the central exchange/clearing house.

As is true with other forms of over-the-counter derivatives, CDS might involve liquidity risk. If one or both parties to a CDS contract must post collateral (which is common), there can be margin calls requiring the posting of additional collateral. The required collateral is agreed on by the parties when the CDS is first issued. This margin amount may vary over the life of the CDS contract, if the market price of the CDS contract changes, or the credit rating of one of the parties changes. Many CDS contracts even require payment of an upfront fee (composed of "reset to par" and an "initial coupon.").[23]

Another kind of risk for the seller of credit default swaps is jump risk or jump-to-default risk.[7] A seller of a CDS could be collecting monthly premiums with little expectation that the reference entity may default. A default creates a sudden obligation on the protection sellers to pay millions, if not billions, of dollars to protection buyers.[24] This risk is not present in other over-the-counter derivatives.[7][24]

Sources of market data

Data about the credit default swaps market is available from three main sources. Data on an annual and semiannual basis is available from the International Swaps and Derivatives Association (ISDA) since 2001[25] and from the Bank for International Settlements (BIS) since 2004.[26] The Depository Trust & Clearing Corporation (DTCC), through its global repository Trade Information Warehouse (TIW), provides weekly data but publicly available information goes back only one year.[27] The numbers provided by each source do not always match because each provider uses different sampling methods.[7] Daily, intraday and real time data is available from S&P Capital IQ through their acquisition of Credit Market Analysis in 2012.[28]

According to DTCC, the Trade Information Warehouse maintains the only "global electronic database for virtually all CDS contracts outstanding in the marketplace."[29]

The Office of the Comptroller of the Currency publishes quarterly credit derivative data about insured U.S commercial banks and trust companies.[30]

Uses

Credit default swaps can be used by investors for speculation, hedging and arbitrage.

Speculation

Credit default swaps allow investors to speculate on changes in CDS spreads of single names or of market indices such as the North American CDX index or the European iTraxx index. An investor might believe that an entity's CDS spreads are too high or too low, relative to the entity's bond yields, and attempt to profit from that view by entering into a trade, known as a basis trade, that combines a CDS with a cash bond and an interest rate swap.

Finally, an investor might speculate on an entity's credit quality, since generally CDS spreads increase as credit-worthiness declines, and decline as credit-worthiness increases. The investor might therefore buy CDS protection on a company to speculate that it is about to default. Alternatively, the investor might sell protection if it thinks that the company's creditworthiness might improve. The investor selling the CDS is viewed as being "long" on the CDS and the credit, as if the investor owned the bond.[8][12] In contrast, the investor who bought protection is "short" on the CDS and the underlying credit.[8][12]

Credit default swaps opened up important new avenues to speculators. Investors could go long on a bond without any upfront cost of buying a bond; all the investor need do was promise to pay in the event of default.[31] Shorting a bond faced difficult practical problems, such that shorting was often not feasible; CDS made shorting credit possible and popular.[12][31] Because the speculator in either case does not own the bond, its position is said to be a synthetic long or short position.[8]

For example, a hedge fund believes that Risky Corp will soon default on its debt. Therefore, it buys $10 million worth of CDS protection for two years from AAA-Bank, with Risky Corp as the reference entity, at a spread of 500 basis points (=5%) per annum.

- If Risky Corp does indeed default after, say, one year, then the hedge fund will have paid $500,000 to AAA-Bank, but then receives $10 million (assuming zero recovery rate, and that AAA-Bank has the liquidity to cover the loss), thereby making a profit. AAA-Bank, and its investors, will incur a $9.5 million loss minus recovery unless the bank has somehow offset the position before the default.

- However, if Risky Corp does not default, then the CDS contract runs for two years, and the hedge fund ends up paying $1 million, without any return, thereby making a loss. AAA-Bank, by selling protection, has made $1 million without any upfront investment.

Note that there is a third possibility in the above scenario; the hedge fund could decide to liquidate its position after a certain period of time in an attempt to realise its gains or losses. For example:

- After 1 year, the market now considers Risky Corp more likely to default, so its CDS spread has widened from 500 to 1500 basis points. The hedge fund may choose to sell $10 million worth of protection for 1 year to AAA-Bank at this higher rate. Therefore, over the two years the hedge fund pays the bank 2 * 5% * $10 million = $1 million, but receives 1 * 15% * $10 million = $1.5 million, giving a total profit of $500,000.

- In another scenario, after one year the market now considers Risky much less likely to default, so its CDS spread has tightened from 500 to 250 basis points. Again, the hedge fund may choose to sell $10 million worth of protection for 1 year to AAA-Bank at this lower spread. Therefore, over the two years the hedge fund pays the bank 2 * 5% * $10 million = $1 million, but receives 1 * 2.5% * $10 million = $250,000, giving a total loss of $750,000. This loss is smaller than the $1 million loss that would have occurred if the second transaction had not been entered into.

Transactions such as these do not even have to be entered into over the long-term. If Risky Corp's CDS spread had widened by just a couple of basis points over the course of one day, the hedge fund could have entered into an offsetting contract immediately and made a small profit over the life of the two CDS contracts.

| This article uses material from the Wikipedia article Metasyntactic variable, which is released under the Creative Commons Attribution-ShareAlike 3.0 Unported License. |